The rise of banking as a service: revolutionising financial services

The global financial services sector has undergone a dramatic transformation, led by technological innovations and changing consumer behaviour. Banking as a service (BaaS) has emerged as one of the most significant advancements. This innovative model is significantly transforming the way financial services are delivered and the way consumers and businesses can access new opportunities through financial products.

What is BaaS?

It is a simplified model of an open banking system that enables entities providing non-banking financial services to access and use a bank’s existing infrastructure and in-house technologies through application programming interfaces (APIs) and other software integrations.

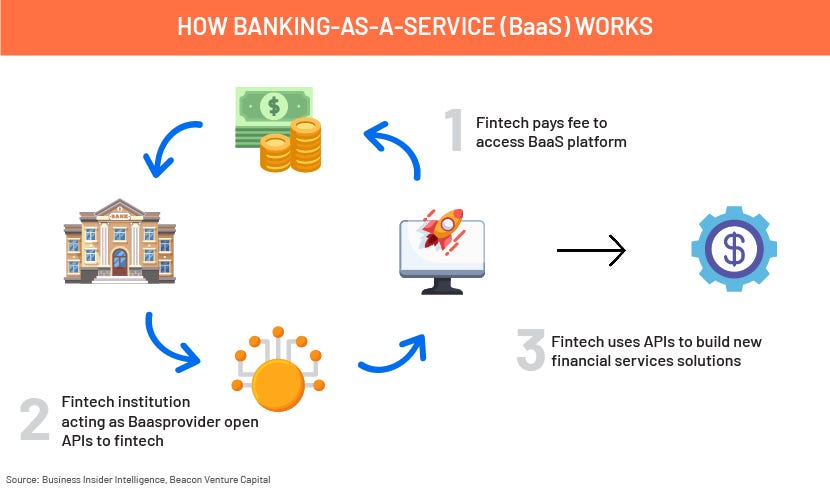

How does BaaS work?

BaaS operates by dissociating banking services from their traditional brick-and-mortar banking infrastructure and offering innovative technological solutions through new channels and products. The following is a simplified breakdown:

Source: Business Insider Intelligence, Beacon Venture Capital

- Partnerships: Licensed banks and BaaS providers partner to share their financial infrastructure and comply with regulations

- APIs: Created by BaaS providers, these enable businesses to incorporate banking features into their applications

- Integration: Non-banking businesses integrate APIs into their platforms to offer banking services to customers, bypassing the complexities of banking infrastructure

- Customer experience: Customers enjoy a continuous banking experience

Why BaaS is a game changer?

The BaaS model is changing the financial services scene in several key ways:

- Innovation and flexibility: BaaS encourages businesses to innovate rapidly and create financial products that suit their customers’ specific needs. “BaaS is helping banks to increase their revenue by almost 2–5% in certain geographies”, according to a report by business management consultant Oliver Wyman.

- Cost-efficiency: Non-banking businesses can substantially reduce their cost of developing and maintaining banking services applications by using existing banking networks and infrastructure. “New BaaS technology can reduce the cost of acquiring a customer from USD100–200 to only USD5–35”, according to a report by Oliver Wyman.

- Financial inclusion: There were 1.4bn who remained unbanked in 2023, according to a World Bank report. BaaS has opened the way for non-traditional players to offer banking services to unbanked or niche markets.

- Faster time to market: Businesses can launch new financial products and services more quickly with the help of BaaS.

- Better customer experience: Better-quality, easy-to-use and newer customised products have improved overall customer experience and loyalty.

A recent survey by Vodeno-Aion Bank of more than 3,000 European customers found that most (52%) 25- to 34-year-olds prefer using financial products and services from their favourite brands than from traditional banks, while 50% will remain loyal only to brands offering embedded financial products and flexible solutions such as buy now, pay later (BNPL) and cashback.

Market size and growth

Market value:

The global BaaS market is valued at approximately USD15bn in 2024, according to IDC. It has grown at a CAGR of 20–25% over the past four years, highlighting the accelerating adoption of BaaS solutions.

The BaaS market is projected to reach around USD45bn by 2028, indicating continued strong growth and the expanding role of BaaS in the global financial ecosystem.

Source: IDC Global Insight report

Real financial world examples

Several companies have already leveraged the BaaS model to disrupt the traditional banking ecosystem:

- Galileo Financial Technologies: Provides a BaaS platform that offers a wide range of banking services through its API infrastructure (source: GFT)

- BBVA Open Platform: Banco Bilbao Vizcaya Argentaria (BBVA) offers BaaS solutions through this platform (source: BBVA)

- Commerzbank: Offers BaaS solutions through its subsidiary, Commerzbank API Marketplace (source: COMZ)

- Standard Chartered: Presents BaaS solutions through its digital banking platform

- Chime: A neobank that extends digital banking services without physical branches, powered by a BaaS model (source: Chime)

- Stripe: Has entered the banking services ecosystem through its BaaS offerings (source: Stripe)

- Solarisbank: Offers a range of banking services through APIs, enabling fintech companies to offer their new financial products efficiently (source: Solarisbank)

The future of BaaS

The future of BaaS will likely be dynamic and transformative. With the evolution of technologies in open banking and artificial intelligence, changing regulatory landscapes and increasing demand for integrated financial solutions, BaaS would continue to shape the financial services sector.

Evolution of open banking: Open banking provides third parties with access to a bank’s customer data, while BaaS enables third parties to access a bank’s functionalities. The adoption of BaaS by banks and third-party non-banks would encourage more open-banking APIs to come to market more quickly, creating a multiplier impact on the banking sector’s changing landscape.

Globalisation of banking services: BaaS will become mainstream in the next two years (by 2026), according to a Gartner report. The study predicts that 30% of banks with assets exceeding USD1bn will introduce BaaS as a means to generate additional revenue by the end of 2024. BaaS would also help in cross-border banking, where advanced banking services will be available to countries in which banking infrastructure is not strong.

How Acuity Knowledge Partners can help

Investment banking outsourcing is becoming a go-to solution to optimize performance and manage risks effectively. With our deep industry research capabilities, we identify early trends in the banking sector and help clients make informed decisions.

Sources:

How the banking-as-a-service industry works and BaaS market outlook for 2021, Shelagh Dolan, 20 July 2021

Banking as a Service Explained, Deloitte Consulting LLP, Andrew Cowley, Tim O’Connor, Neil Malani, Gys Hyman, July 2021

Banking as a Service vs. Open Banking vs. Platform Banking. What Are They and What Are They Not?, Maryna Cherednychenko, 23 April 2021

- Bank as a Service and Open Banking Models Explained, SEPA Cyber Technologies

- The Evolution of Banking: 2021 and Beyond, Jim Marous

- Gartner report: Banking-as-a-Service Will Hit Mainstream Adoption Within Two Years

- IDC research report: Future-Ready Payments Platforms Enabling the Next Phase of Growth for Banks

Abhisek Sasmal has over 14 years of work experience in equity and macro research, financial and credit risk modelling. Currently, he is supporting a European buy-side client mainly in the diversified financial sector. He has been with Acuity for the last 13 years supporting Global Fund Managers and sell-side analysts in their research on Global BFSI. He is an MBA in finance and a CFA charter holder. Before joining Acuity Knowledge Partners, he used to work with some leading domestic sell-side firms in India on diversified sectors.